Seven Heavens of Finance and the Open Risk API

Back-to-basics is not salvation

It has become trendy since the financial crisis to be wearing an anti-complexity hat in matters concerning the shape of the financial system. This is an understandable reaction to the entangled constructions that had sprung to existence in the hyper-leveraged markets of the naughty noughts.

Yet shifting through the ruminations and proclamations one cannot help but get the impression that there is a sort of denial of the complexity that underlies the real economy. One gets the impression that people are harking back to a simplicity that does not exist. Since the financial system must at least support the actual economy, we would suggest that

Finance cannot be simpler than the economy it serves

So let us, for argument’s sake, remove all complicated interest rate derivatives, repackaging of securities, high frequency trading, peer-to-peer lending and other bitcoin inventions. Is the resulting financial system actually simple and do we know how to risk manage it effectively?

Just how complicated is the financing of the real economy?

Let us explore a case of simple bricks and mortar finance. We will consider a generic commercial bank. Its managers are jolly good fellows, proverbial golf players, that do not delve in the aforementioned weapons of mass destruction. Let us further assume that they finance (among other real economy projects) commercial real estate. That is, they simply lend money to companies that own commercial buildings (lets say office space) and use such property as collateral for their loans.

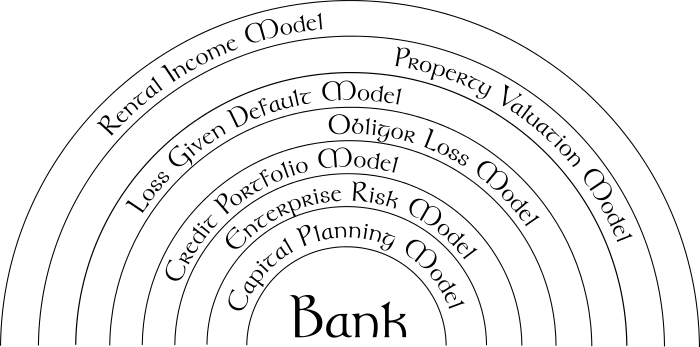

So what kind of universe do these honorable men live in? How complex is it to risk manage that system and on the basis of what information (data) and risk models? Well, the summary news report says that this simplest of cases is actually a universe with at least seven layers of complexity. Here is the breakdown:

The First Heaven: The Asset Cash flow Risk Layer

Our first heavenly sphere is appropriately close to the ground: Buildings must be leased to companies to earn rents (which among others will also help repay the loan). There is a myriad or risk (uncertainty) factors that influence the actual rent that will be earned by the property. Starting with the attributes and condition of the property itself, its location, business demand for office space and competing offerings, the economic health of the tenants, the prevailing interest rates and so on and so forth. Somewhere, somehow a poor banker has to collect all these numbers and assumptions (typically in an excel sheet) to try to understand this most fundamental risk factor.

The Second Heaven: The Asset Valuation Risk Layer

The second Heaven floats closely above the first one, but has a distinctly different air quality. Cash flows are very informative, but we need to get a magical transformation of the numerous possible projections into a single number: the property value. This is because there is a critical number we need to establish, the so-called Loan to Value ratio. Since a building will typically not be listed and actively traded in any market, how is this value to be determined? This is typically done with a valuation model, using the cash flow projections of the previous layer but also further inputs, for example from market transactions. This establishes a risk premium with which to discount the previously modeled cash flows.

The Third Heaven: The Loss-Given-Default Risk Layer

The third Heaven is simply the projection of the second (valuation) layer into specific states of the future. For our little commercial bank, what really matters is not the current value of the property but its value at a time point where the loan might stop being serviced. That scenario is when the property might be used as a means to mitigate loss on the loan.

Such future value estimates could be based on the projected remaining future cashflows conditional on such an event and reflecting the prevailing market risk premia on that occasion (e.g., will it be a singular event or a market rout)? Yet this approach entails far too many assumptions and it is at this layer where we have the first methodological pivot and effectively a complexity cover up. Namely instead of continuing with a bottom up approach for a recovery model for the actual property / loan, there is typically a switch to estimating recovery rates from historical data. The price to pay is that such data might not be representative, not nearly sufficient statistically and may not provide enough information on stressed recovery rates.

The Fourth Heaven: The Borrower Default Risk Layer

The bank doesn’t really care about property valuations and recoveries per-se, unless that is, the borrower gets in financial difficulty. When and why a borrower may get into such a condition is a fairly complicated story: The quality of the rental income is a key factor, but the borrower may be running other risks besides this particular building (they may also have other financial resources).

We need a model for the likelihood that the borrower will get into difficulty, given all their assets, liabilities, guarantees etc. This task is getting increasingly dire, as we probably don’t know all the relevant details about the borrower. We conveniently abstract into their various operations into a single entity, and we hope the tangled web of ownership can be captured in a simplified view of a single probability of default (or PD). In common practice the risk horizon does not even exceed a one-year forward estimate.

The Fifth Heaven: The Portfolio Management Layer

It would be a strange bank if its only business purpose would be to lend funds against a single property. The fifth heaven is where all the different lending projects of the bank meet each other. Some loans may be financing other real estate firms, others might be advanced in completely different parts of the economy. We can subdivide this layer if we wish, say into business sectors and regions. But this would only make the real economy appear more complex.

Our information requirements have gone up by one or more orders of magnitude, depending on the size of the portfolio. We now need to get a handle on the joint credit performance of all these different projects in different scenarios.

Yet another abstraction and simplification is in order: Instead of stressed loss estimates for each individual borrower we might simply bundle loans together into a pool and work with the fractional loss rate of the pool instead.

The Sixth Heaven: The Enterprise Risk Management Layer

It would be a heavenly gift if all these portfolio loans could somehow be originated, processed and serviced by an infallible, indestructible, dispassionate and trusted AI, but in reality the business of lending is still done by earthen creatures. Which means for example that people might occasionally develop fraudulent tendencies from within. More typically our mom-and-pop lending operation is also exposed to outside fraud, interest rate risks, liquidity mismatches of loans being advanced and prepaid, and countless other risk types that are not core to the credit provision.

Yet these risks are not separable from the lending activity and must be managed. Getting a grip on these risks requires to bring in further information about the bank itself, its business model, its people, its systems and processes and finally integrating all that information into one grant view. The availability of enterprise risk models is still on the wish list for most banks.

The Seventh Heaven: The Regulatory Capital Layer

We have finally reached the seventh Heaven, which is inhabited by wise and erudite beings (lets call them Controllers or Regulators) which hover way above the fray. They inspect the state of the economic universe and pull or push large levers covered with runic engravings. Their objective is to keep the heavenly spheres rotating smoothly. It is indeed a very awkward moment if there is an unexpected jolt in the system and the financial spheres screech to a halt. Heaven-forbid, this would suggest that, despite the ritual and the pomp, there is actually little real control of the system.

To prevent such unpleasantness, Controllers and Regulators continuously talk to the jolly-good-fellow bank managers and ask them to provide estimates projecting how the lower spheres will evolve in future scenarios and, importantly, how they will respond to unforeseen adversity. The bank managers themselves and their management strategies become part of the model. Alas, even the simplest such questions need a major effort for the query to round-trip to the bottom layer and then back up. The accuracy of the signal as it propagates through layers and layers of information loss is only to be guessed at.

If a state is not observable, the Controller will never be able to determine the behavior of an unobservable state and hence cannot use it to stabilize the system

A good deal of complexity is here to stay

We can go back to these seven layers and check whether we can simplify the structure, shorten the communications, reduce the signal loss or enhance the observability. Complexity reduction does not seem likely except at the margin. You can repackage loans into securities (aka: banking versus capital markets channels). This simply changes the agent that is responsible for risk management and where portfolio diversification takes place. You can try to trade off bank size with bank number for similarly ambiguous benefits. By and large we must accept that there is an irreducible amount of complexity that characterises even the most basic and indispensable financing business. Yet ensuring control of the system requires observability. How do we achieve it?

This is a good time for information engineers

Ultimately we must face the fact that a well functioning financial system needs a sizeable amount of financial engineering technology, which is essentially specialized information technology. The main challenge in the above real life example of commercial real estate lending is ensuring that information is acquired, processed, propagated and aggregated in an efficient and validated manner, not necessarily always within the same firm or entity.

This is primarily a question of standards, formats and protocols for exchanging financial information for risk management purposes. Similarly, there is a need to document far more thoroughly the layers of risk modelling that is being performed and used in decision-making. Finally, observability and control are enhanced by ensuring that key data (that are not proprietary and ring-fenced for privacy or commercial secrecy reasons) are openly accessible.

One of the most powerful information technology tools to help with this task is to develop an application programming interface (API) for the communication and documentation of risk data and risk models. This is why we are excited about and continue developing the Open Risk API