Risk Management Skills for the Fintech Era

Financial services jobs continue being decimated. A recent (as of the initial post date) FT article was a sobering summary of the continuing transformation of the financial sector: 2015 alone has seen more than 10% reduction of the total workforce across large EU/US banks:

As main drivers for this true jobs hecatomb are cited higher minimum capital requirements (that depress Return on Equity and hence require lower costs to restore it to investor acceptable levels), low interest rates that erode Profitability Margins, and a generally subdued economic landscape which reduces Volumes.

The economic outlook is still a bit away from being glowing. The ongoing digital transformation of financial services adds a further (profoundly structural) driver that will lead to much further reshaping of the jobs required in banking. In fact, it is likely we have not seen anything yet from the full impact of digital technologies.

The infiltration of digital in finance will be unusually high, because when striped from its glass towers and other pomp,

a bank is, in essence, an IT platform to help risk managers intermediate financial activity in a sustainable manner

If the above summary is true (old style bankers certainly did not see things this way), growth and jobs will accrue to the organizations and individuals that internalize this core reality and prepare themselves accordingly.

The current Fintech scene is but the thin edge of a wedge

There is deafening marketing noise from the fintech scene these days. It is amplified by generous venture capital funding and the need for early investors to make an exit before the current valuation froth evaporates. From the amount of publicity one might surmise we are already in a five-to-twelve moment, just before the infamous disruption event.

Yet upon calm closer inspection one realizes that the existing fintech landscape is generally opportunistic (e.g., focusing on low-hanging fruit associated with customer preferences around mobile devices) and is actually an enormously incomplete approach to financial services provision.

In particular the fintech relationship with risk management, in our view a key ingredient for any realistic new take on financial service offering is sketchy at best.

The pitches make, for example, vague references to sophisticated algorithms for improved risk selection. This is ominously off the mark given that the banking industry is full of scars from its toying with double-edged quantitative risk models. Who knows, maybe artificial intelligence (A.I.) will indeed succeed where our lowly carbon based human intelligence failed again and again. In that case the future bank may turn in a pure an IT platform and its human payroll will actually have zero (0, nada, none) jobs. Except, hopefully, one stand-by person to push the power-off button when things go awry (lets call her the human risk manager of last resort).

On the flipside, and back to the current human reality, fintech is exposed to aggravated data privacy and cybersecurity risks. For risk managers the only true dilemma is really:

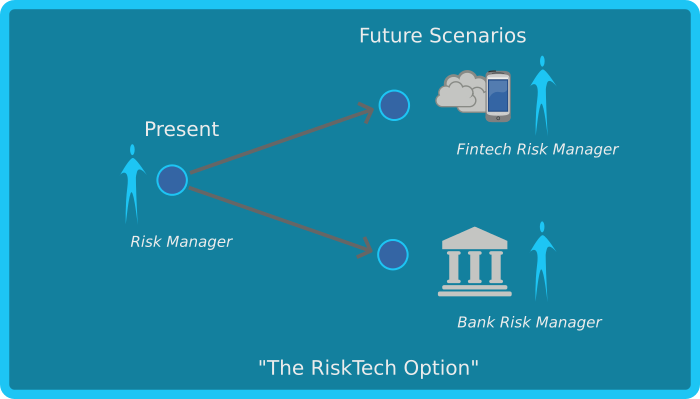

Do you build out next generatio risk management capability modifying the old IT platform or do you start fresh with a new IT platform

No matter what you choose, life has cut out the work for you:

The Banana Skins that are not going away

The long-running CSFI/PwC Banana Skins study offers a useful summary of risk management challenges. It is useful to study it to see what risk management capabilities are being required going forward. (While one may not necessarily agree with the selection of risks and the ordering of importance, it is a good reference point for what the financial industry might be needing in terms of skills in order to meet its risk management challenges.)

Let’s look at them banana skins (based on the last survey, 2015) in sequence, along with an assessment of the skills implications for risk managers:

- Macroeconomic Risks: Identifying economic dynamics at the highest aggregation level and translating it to the risks and opportunities for the firm. Relevant Risk Management Job skills: Qualitative and Quantitative Economic Analysis, Stress Testing, Portfolio Management

- Cybercrime: Identifying vulnerabilities and protecting the firm’s IT platform from external attack. Relevant Risk Management Job skills: Digital Communication Technology, Encryption Methods, Client Behaviours

- Regulation: Ability to efficiently implement regulations to ensure confidence in the firms ability to operate safely. Relevant Risk Management Job skills: Risk Culture, Risk Appetite, Capital Management, Risk Data

- Technology: Identifying risks and opportunities in utilizing emerging technologies for efficient and sustainable financial service provision. Relevant Risk Management Job skills: Datacenters (NoSQL databases, Big Data), Cloud, Open Source, Mobile clients (lets add Blockchain as well for completeness!)

- Political Risk: Managing the relationship with broader set of stakeholders. Relevant Risk Management Job skills: Sustainability, Transparency

- Quality of Risk Management: Improving the quality of risk managers and risk management processes and tools. Relevant Risk Management Job skills: Standardization, Peer Review / Benchmarking

- Credit Risk: Identifying risks and opportunities when lending to sovereigns, businesses and consumers. Relevant Risk Management Job skills: Individual Risk Assessment, Sectoral Risk Correlations, Feedback Loops (Risk Contagion)

- Conduct Risk: Identifying and controlling risks associated with poor business practices. Relevant Risk Management Job skills: Employee Incentives, New Product Risks, Client Relationships

- Mis-Pricing Risk: Ensuring there is adequate return for underwritten risks. Relevant Risk Management Job skills: Portfolio Management, Risk-Adjusted Pricing

- Business Risk: Identifying risks and opportunities in achieving sustainable business models: Relevant Risk Management Job skills: Business Model Analysis, Client Behaviours

A daunting laundry list for sure. Getting on top of those risks is not optional, though. There will be many associated job opportunities, if not actual shortage of well-trained risk management personnel.

The narrow talent pool, or why no kid wants to become a risk manager

Risk management, in general, is a still nascent discipline. It is not taught at schools except as a specialist post-graduate option at the end of university level education. It gets oversimplified as the art of saying no, when it actually promotes rigorous understanding of the full range of outcomes. In firms, it is frequently a second class support function, on the assumption that the real risk management is practiced elsewhere. The people we would identify as Risk Management Heroes would probably not label themselves as risk managers.

Recognizing that risk management is one of the core competencies of banks will do wonders to its prestige. In any case,

Just as fintech is the response to poor technology standards, RiskTech is the response to poor risk management standards

The premise is that if current financial sector players have difficulty implementing a sustainable, risk management oriented IT platform, new players might have a better chance. So old and new risk managers rejoice! Whether you chose to work with old iron or shiny new kit, your skills are needed more than ever. This is an option, the risktech option, and as you surely know, options are valuable!

At Open Risk our mission is to help you realize and maximize this option:

- We developed a computational credit portfolio management platform OpenCPM which makes transparent (open data and open source based) credit portfolio analytics available on-line.

- We offer the Open Risk Academy which provides easy access to interactive risk management training.

- We sponsor the free and open collection of collaborative tools in the Open Risk Manual which makes available to the risk managers everywhere a wide array of web based and community driven, resources.