Four individuals that can look straight into your eyes Here are four individuals that can look straight into your eyes

Torvalds developed the #linux operating system, the software engine now powering anything from the tiniest #raspberrypi to the scariest supercomputer. Humanity’s best guarantee that the digital era remains an equal playing field Mullenweg developed the #wordpress blogging platform. Gave voice and content ownership to millions of digital authors making him the closest to the Gutenberg of our era Dougiamas developed #moodle, the world’s digital Academy.

Transition Matrix Library First Release Open Risk released version 0.1 of the Transition Matrix Library

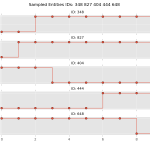

Motivation State transition phenomena where a system exhibits stochastic (random) migration between well-defined discrete states (see picture below for an illustration) are very common in a variety of fields. Depending on the precise specification and modelling assumptions they may go under the name of multi-state models, Markov chain models or state-space models.

In financial applications a prominent example of phenomena that can be modelled using state transitions are credit rating migrations of pools of borrowers.

Loan Level Templates Using Python In this Open Risk Academy course we figure step by step how to use python to work with Loan Level Templates, using the ECB SME template as an example.

Overview of the loan level template Manipulating spreadsheets with Python The Python Dictionary Organization of Portfolio Data Generating Test Portfolios Get an Open Risk Academy account and get started with the course here

This blog has been verified by Rise: Rcf8d5e45f6964ba5d03bda4020a97dda

Transparency, collaboration key to regaining trust in financial services In banking, confidence is the first order of business Maintaining the confidence of market participants, clients, shareholders, regulators and governments is uniquely important for the financial sector. Trust is, quite literally, the real currency. Yet it is a truism that confidence is hard to build up and rather easy to destroy. Why is this so?

The short answer: The difficulty in rebuilding trust is linked to the lack of transparency.

How much digital bank can we fit in a 50 euro bill? Much has been said about the impact of Big Data and high-end GPU computing on the provision of digital financial services. At Open Risk we wanted to explore the boundary of what is possible at the diametrically opposite end of the cost spectrum:

What is the_absolutely minimum_cost for providing digital financial services? . In this post we begin the journey of finding out the answer to that question and it promises to be fascinating!

Risk Management Internship In finance, it’s the best of times, it’s the worst of times It is a special moment to start a career in financial services. We are walking amid the ruins of the previous financial order. Fallen banks, broken markets, negative interest rates, shell-shocked economies and discredited theoretical assumptions. We see the enormous cost and impact to the welfare of society of a less than perfect financial system which has not kept pace with the advancement of our general knowledge and technical capabilities in most other domains.

Open Risk is proud to be funded by the FIWARE FINODEX accelerator!

Finodex, the European accelerator for ICT projects based on Open Data and FIWARE technologies, has already chosen over one hundred projects via two open calls for proposal.

This week the results of the second call evaluation closed in last September have been published, and 52 projects from a total of 297 have been chosen by a panel of experts.

Open Risk API If you work in financial risk management you will most likely recognize where the following sentence is coming from:

One of the most significant lessons learned from the global financial crisis that began in 2007 was that banks information technology (IT) and data architectures were inadequate to support the broad management of financial risks. This had severe consequences to the banks themselves and to the stability of the financial system as a whole For those lucky few risk managers not being affected by inadequate IT systems, the excerpt is from the Basel Committee’s Principles for effective risk data aggregation and risk reporting (2013).

Risk modeling is as much art as it is science The Zen of Modeling aims to capture the struggle for risk modeling beauty

An undocumented risk model is only a computer program A risk model that cannot be programmed is only a concept A risk model only comes to life with empirical validation Correct implementation of an imperfect model is better than wrong implementation of a perfect model In complex systems there is always more than one path to a risk model There are no persistently true models but there are many persistently wrong models Correlation is imperfectly correlated with causation Nirvana is the simplest model that is fit for purpose Hierarchical systems lead to hierarchical models.

The four stages of social Homo Staticus The web as we now know it burst first into the open in the early nineties. It certainly did not start among the more socially active classes. It was an invention by and for nerdy CERN physicists, to exchange data about elementary particle experiments. But it wasn’t long before academics figured out additional valuable uses of this technology: You could put your face online, along with a CV.

Revisiting simple concentration indexes Our white paper Revisiting simple concentration indexes reviews the definitions of widely used concentration metrics such as the concentration ratio, the HHI index and the Gini and clarify their meaning and relationships.

This new analytic framework helps clarify the apparent arbitrariness of simple concentration indexes and brings to the fore the underlying unifying concept behind these metrics, thereby enabling their more informed use in portfolio and risk management applications.

This page is a summary of a presentation given at the 2014 Autumn TopQuants Meeting, aka, the Open Source Risk Modeling Manifesto.

The dismal state of quantitative risk modeling The current framework of internal risk modeling at financial institutions has had a fatal triple stroke. We saw in quick sequence: market risk, operational risk, and credit risk measurement failures, covering practically all business models.

This fact left the science and art of quantitative risk modeling reeling under the crushing weight of empirical evidence.

Financial Risk Modelling has suffered enormous setbacks in recent years, with all major strands of modelling (market, credit, operational risk) proven to have debilitating limitations. It is impossible to imagine a modern financial system that does not make extensive use of risk quantification tools, yet rebuilding confidence that these tools are fit-for-purpose will require significant changes. These need to improve governance, transparency, quality standards and in some areas even the development of completely new strands of modelling.

Open Risk Presentation summarizing the Public Beta Phase Overview of the motivation for initiating Open Risk and the solutions being delivered in the current phase.

Venue: Online Location: The world Time: September 18th 2014 Link to presentation: Open Risk Overview

The first batch of open source tools focusing on Credit Portfolio calculations is now available here. The functionality aims to standardize Name Concentration Measurement (concentrationMetrics)