What do we mean by credit data? This post is a discussion around mathematical terminology and concepts that are useful in the context of working with credit data, taking us from network graph representations of credit systems to commonly used reference data sets

Course Objective Digging into the meaning of credit data collections, the logic that binds them together towards understanding what they can be used for and what limitations and issues they may be affected by, this new course in the Credit Portfolio Management category explores a new angle to look at an old practice.

The course is now live at the Academy.

Pre-requisites Familiarity with credit provision in general (lending products, banking processes and credit risk) is required for getting the most out of the course.

Solstice is a flexible open source economic network simulator. Its primary outcomes are quantitative analyses of the behavior of economic systems under uncertainty. In this post we provide a first overall description of Solstice to accompany the first public release.

Modeling economic networks and their dynamics Economic networks are the primary abstractions though which we can conceptualize the state (condition) and evolution of economic interactions. This simply reflects the fact that human economies are quite fundamentally systems of interacting actors (or nodes in a network) with transient or more permanent relations between them.

In practice the network character of an economy is frequently suppressed or under-emphasized and does not play a particularly important role.

What is the future of stress testing? To speculate on the future of Stress Testing we need first a basic definition what stress testing is. Broadly speaking, the goal of Stress Testing is to assess how a system would behave under adverse conditions that - while not the most likely outcome with the knowledge of today - are within the realm of the plausible.

There are, broadly speaking, two types of stress testing: The Real stress testing version and Hypothetical stress testing version.

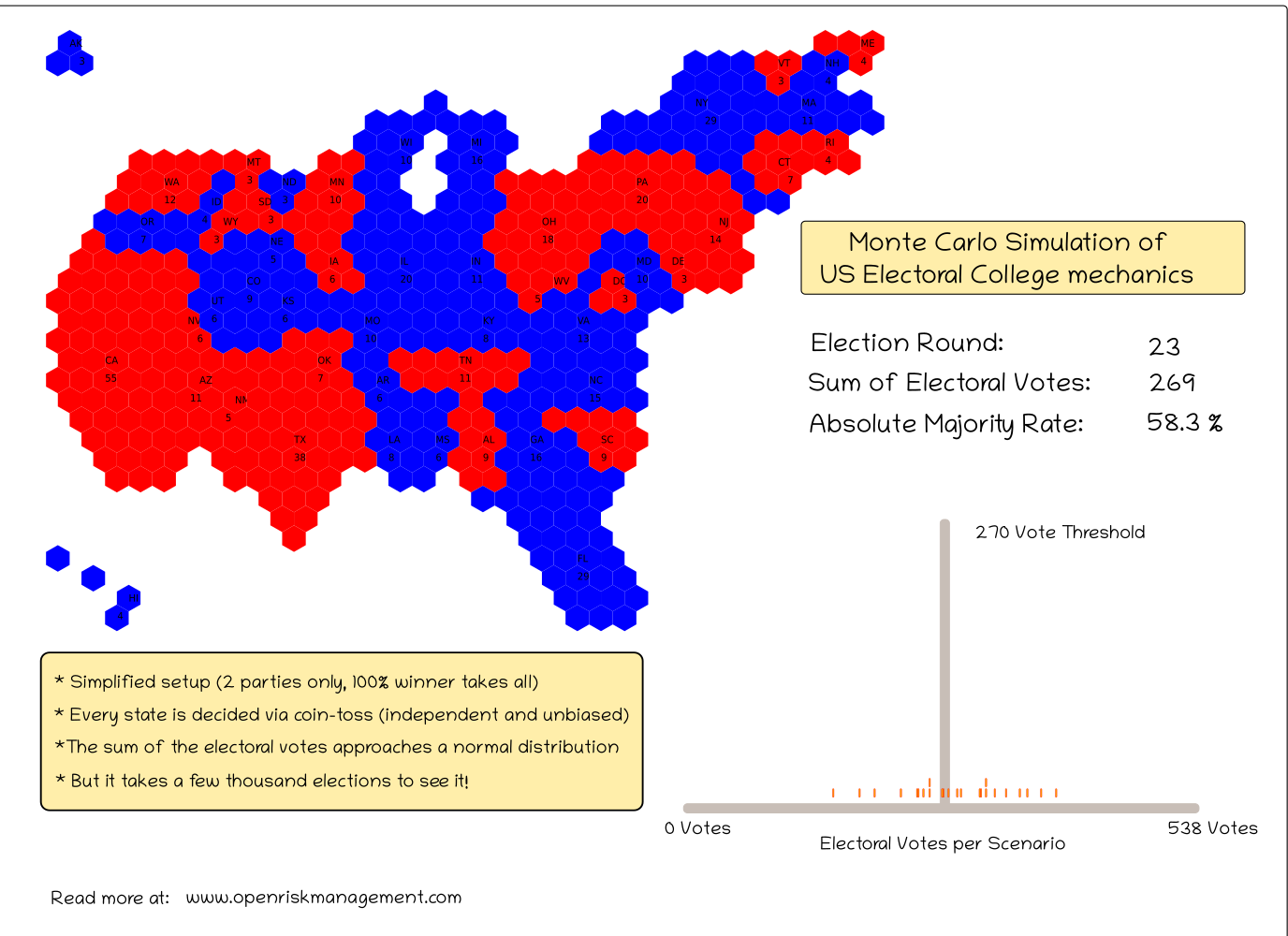

Using a simplified version of the rules of the US Electoral College system we illustrate how the use of Monte Carlo techniques allows exploring systems that show combinatorial explosion

The role of simulation in risk management and decision support A Simulation is a simplified imitation of a process or system that represents with some fidelity its operation over time. In the context of risk management and decision support simulation can be a very powerful tool as it allows us to assess potential outcomes in a systematic way and explore what-if questions in ways that might otherwise be not feasible. Simulation is used when the underlying model is too complex to yield explicit analytic models (An analytic model is one can be “solved” exactly or with standard numerical methods, for example resulting in a formula).

Agent-Based Models The origins and early years According to Wikipedia an agent-based model (ABM) is

ABM: class of computational models for simulating the actions and interactions of autonomous agents (both individual or collective entities such as organizations or groups) with a view to assessing their effects on the system as a whole. A cellular automaton is a particular class of ABM. It is a discrete dynamical model used and studied in a variety of fields: computer science, mathematics, physics, complexity science, theoretical biology among others.

Course Content This course is an introduction to the concept of credit contagion. It covers the following topics:

Contagion Risk Overview and Definition Various Contagion Types and Modelling Challenges The Simple Contagion Model by Davis and Lo Supply Chains Contagion Sovereign Contagion Who Is This Course For The course is useful to:

Risk Analysts across the financial industry and beyond Risk Management students Quantitative Risk Managers developing or validating risk models How Does The Course Help Mastering the course content provides background knowledge towards the following activities:

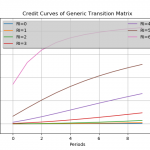

Release of version 0.4.1 of the transitionMatrix package focuses on stressing transition matrices Further building the open source OpenCPM toolkit this realease of transitionMatrix features:

Feature: Added functionality for conditioning multi-period transition matrices Training: Example calculation and visualization of conditional matrices Datasets: State space description and CGS mappings for top-6 credit rating agencies Conditional Transition Probabilities The calculation of conditional transition probabilities given an empirical transition matrix is a highly non-trivial task involving many modelling assumptions.

Release of version 0.4 of the transitionMatrix package Further building the open source OpenCPM toolkit this realease of transitionMatrix features:

Feature: Added Aalen-Johansen Duration Estimator Documentation: Major overhaul of documentation, now targeting ReadTheDocs distribution Training: Streamlining of all examples Installation: Pypi and wheel installation options Datasets: Synthetic Datasets in long format Enjoy!

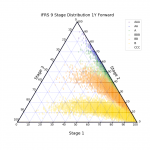

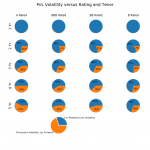

Is the IFRS 9 or CECL standard more volatile? Its all relative Objective In this study we compare the volatility of reported profit-and-loss (PnL) for credit portfolios when those are measured (accounted for) following respectively the IFRS 9 and CECL accounting standards.

The objective is to assess the impact of a key methodological difference between the two standards, the so-called Staging approach of IFRS 9. There are further explicit differences in the two standards.

Credit Portfolio PnL volatility under IFRS 9 and CECL Objective We explore conceptually a selection of key structural drivers of profit-and-loss (PnL) volatility for credit portfolios when profitability is measured following the principles underpinning the new IFRS 9 / CECL standards

Methodology We setup stylized calculations for a credit portfolio with the following main parameters and assumptions:

A portfolio of 200 commercial loans of uniform size and credit quality Maturities extending from one to five annual periods A stylized transition matrix producing typical multiyear credit curves Correlation between assets typical for a single business sector and geography portfolio Focusing on PnL estimates one year forward, with PnL being impacted both by Realized Losses (defaults) and Provision variability (both positive and negative).

Credit Portfolio Management in the IFRS 9 / CECL and Stress Testing Era The post-crisis world presents portfolio managers with the significant challenge to asimilate in day-to-day management the variety of conceptual frameworks now simultaneously applicable in the assessment of portfolio credit risk:

The first major strand is the widespread application of regulatory stress testing methodologies in the estimation of regulatory risk capital requirements The second major strand is the introduction of new accounting standards (IFRS 9 / CECL) for the measurement and disclosure of expected credit losses While both Regulatory Stress Testing and IFRS 9 / CECL accounting require investment in analytic capabilities and provide unique new insights, both are aimed at satisfying evolving prudential or investor disclosure requirements.

The new IFRS 9 financial reporting standard IFRS 9 (and the closely related CECL) is a brand new financial reporting standard developed and approved by the International Accounting Standards Board (IASB).

Strictly speaking IFRS 9 concerns only the accounting and reporting of financial instruments (e.g. bank loans and similar credit products). Yet the introduction of the IFRS 9 standard has significant repercussions beyond financial reporting, and touches e.g., bank risk management as well.

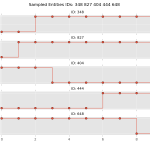

Transition Matrix Library First Release Open Risk released version 0.1 of the Transition Matrix Library

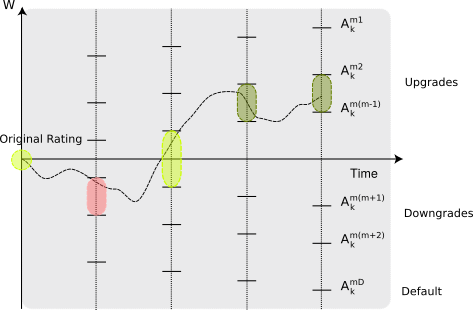

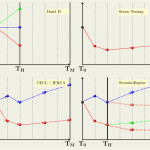

Motivation State transition phenomena where a system exhibits stochastic (random) migration between well-defined discrete states (see picture below for an illustration) are very common in a variety of fields. Depending on the precise specification and modelling assumptions they may go under the name of multi-state models, Markov chain models or state-space models.

In financial applications a prominent example of phenomena that can be modelled using state transitions are credit rating migrations of pools of borrowers.

The Zen of IFRS 9 Modeling At Open Risk we are firm believers in balancing art and science when developing quantitative risk tools. The introduction of the IFRS 9 and CECL accounting frameworks for reporting credit sensitive financial instruments is a massive new worldwide initiative that relies in no small part on quantitative models. The scope and depth of the program in comparison with previous similar efforts (e.g. Basel II) suggests that much can go wrong and it will take considerable time, iterations, communication and training to develop a mature toolkit that is fit-for-purpose.

Accounting probably would not count among the more glamorous of professions. The reasons for that status and whether it is justified are beyond the scope of this brief commentary.

What is interesting to note, though, is that the relative attractiveness of accounting is arguably improving, driven by a number of systemic societal developments:

the need for more proactive assessment of the state of the world, eliminating the infamous “rear-view mirror” pathology.