Stressing Transition Matrices

Page content

Release of version 0.4.1 of the transitionMatrix package focuses on stressing transition matrices

Further building the open source OpenCPM toolkit this release of transitionMatrix features:

- Feature: Added functionality for conditioning multi-period transition matrices

- Training: Example calculation and visualization of conditional matrices

- Datasets: State space description and CGS mappings for top-6 credit rating agencies

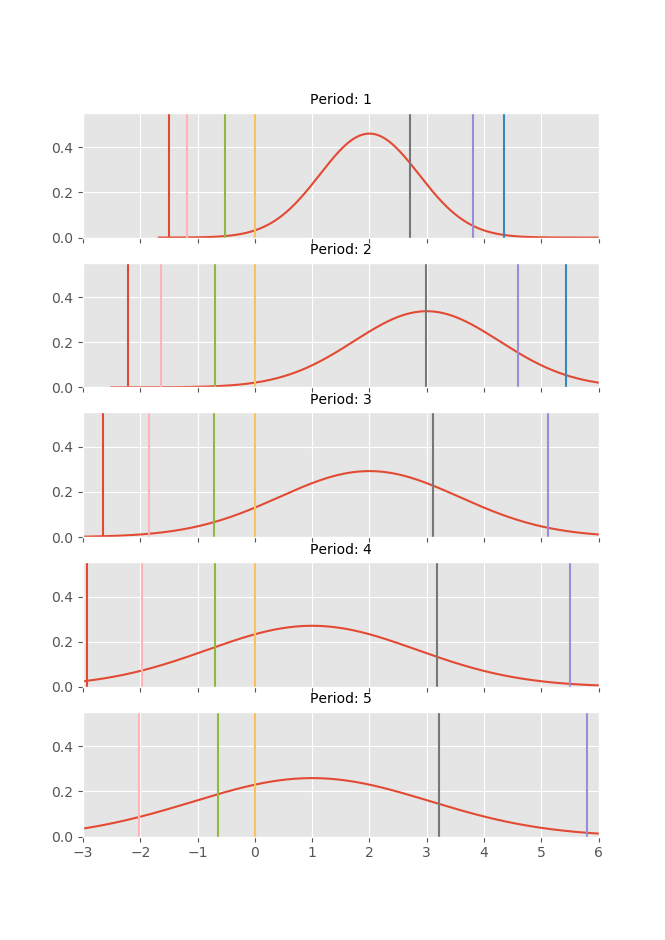

Conditional Transition Probabilities

The calculation of conditional transition probabilities given an empirical transition matrix is a highly non-trivial task involving many modelling assumptions. This version of the transitionMatrix includes a canonical implementation that assumes a Gaussian single factor process as the driver of the joint rating dynamics. The technical documentation is available under in Open Risk Manual under the transition matrix category.

Predefined Credit Rating System Descriptions

This release includes also the state space description (labels, mappings to CQS etc.) for the six largest credit rating agencies (NB: by European market share)

Enjoy!

Comment

If you want to comment on this post you can do so on Reddit or alternatively at the Open Risk Commons. Please note that you will need a Reddit or Open Risk Commons account respectively to be able to comment!