Stress Testing of the Future - A view from 2031

What is the future of stress testing? We speculate on how stress testing might look like in 2031

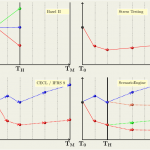

What is the future of stress testing?

To speculate on the future of Stress Testing we need first a basic definition what stress testing is. Broadly speaking, the goal of Stress Testing is to assess how a system would behave under adverse conditions that - while not the most likely outcome with the knowledge of today - are within the realm of the plausible.