The Non-Perfoming Loan Ontology The Non-Performing Loan Ontology is a framework that aims to represent and categorize knowledge about non-performing loans using semantic web information technologies. Codenamed NPLO, it codifies the relationship between the various components of a Non-Performing Loan portfolio dataset.(NB: Non-performing loans are bank loans that are 90 days or more past their repayment date or that are unlikely to be repaid, for example if the borrower is facing financial difficulties).

Non-Performing Loans The covid-19 crisis will certainly impact the concentration of Non-Performing Loans but given the special nature of this economic crisis compared (in particular) with the 2008 financial crisis it is unclear how precisely things will evolve.

In a previous post and white paper (OpenRiskWP07_022616) we discussed the importance of advancing open and transparent methodologies for managing the risks associated with such credit portfolios. Effective management of NPL is also a top regulatory priority.

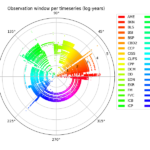

The community mobility reports and OpenCPM In a previous post we introduced new OpenCPM functionality that integrates COVID-19 community mobility data (currently from Google). The reports chart movement trends over time by geography, across different categories of places such as retail and recreation, groceries and pharmacies, parks, transit stations, workplaces, and residential.

While these reports are unlikely to persist as open data sources in the long term, the current availability (as of May 2020) enables providing within OpenCPM a mobility data dashboard that can help draw insights through visualization and statistical analysis.

The community mobility reports and OpenCPM As the COVID-19 pandemic unfolded technology providers (most notably Google and Apple) made available to the public aggregated and anonymized data about human mobility in the crisis period (on the basis of smartphone location data). These Community Mobility Reports provide insights into how mobility patterns changed in response both to pandemic news and policies aimed at combating COVID-19.

The reports chart movement trends over time by geography, across different categories of locations and activities, such as retail and recreation, groceries and pharmacies, parks, transit stations, workplaces, and residential.

Visualization of large scale economic data sets Economic data are increasingly being aggregated and disseminated by Statistics Agencies and Central Banks using modern API’s (application programming interfaces) which enable unprecedented accessibility to wider audiences. In turn the availability of relevant information enables more informed decision-making by a variety of actors in both public and private sectors. An excellent example of such a modern facility is the European Central Bank’s Statistical Data Warehouse (SDW), an online economic data repository that provides features to access, find, compare, download and share the ECB’s published statistical information.

The challenge with historical credit data Historical credit data are vital for a host of credit portfolio management activities: Starting with assessment of the performance of different types of credits and all the way to the construction of sophisticated credit risk models. Such is the importance of data inputs that for risk models impacting significant decision-making / external reporting there are even prescribed minimum requirements for the type and quality of necessary historical credit data.

Release of version 0.4.1 of the transitionMatrix package focuses on stressing transition matrices Further building the open source OpenCPM toolkit this realease of transitionMatrix features:

Feature: Added functionality for conditioning multi-period transition matrices Training: Example calculation and visualization of conditional matrices Datasets: State space description and CGS mappings for top-6 credit rating agencies Conditional Transition Probabilities The calculation of conditional transition probabilities given an empirical transition matrix is a highly non-trivial task involving many modelling assumptions.

Release of version 0.4 of the transitionMatrix package Further building the open source OpenCPM toolkit this realease of transitionMatrix features:

Feature: Added Aalen-Johansen Duration Estimator Documentation: Major overhaul of documentation, now targeting ReadTheDocs distribution Training: Streamlining of all examples Installation: Pypi and wheel installation options Datasets: Synthetic Datasets in long format Enjoy!

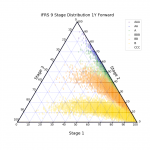

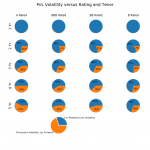

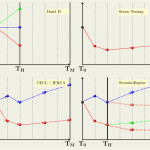

Is the IFRS 9 or CECL standard more volatile? Its all relative Objective In this study we compare the volatility of reported profit-and-loss (PnL) for credit portfolios when those are measured (accounted for) following respectively the IFRS 9 and CECL accounting standards.

The objective is to assess the impact of a key methodological difference between the two standards, the so-called Staging approach of IFRS 9. There are further explicit differences in the two standards.

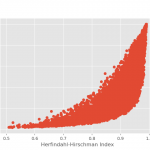

Release of version 0.4 of the Concentration Library adds Geographic / Industrial concentration indexes Further building out the OpenCPM set of tools, we release version 0.4 of the Concentration Library, a python library for the computation of various concentration, diversification and inequality indices.

The below list provides documentation URL’s for each one of the implemented classic indexes (the Hoover index is a new addition in this release)

Atkinson Index Hoover Index Concentration Ratio Berger-Parker Index Herfindahl-Hirschman Index Hannah-Kay Index Gini Index Theil Index Shannon Index Generalized Entropy Index Kolm Index An important new direction that appears first in this release is the introduction of indexes that measure geographical and industrial concentration.

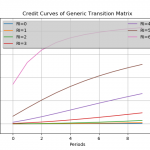

Credit Portfolio PnL volatility under IFRS 9 and CECL Objective We explore conceptually a selection of key structural drivers of profit-and-loss (PnL) volatility for credit portfolios when profitability is measured following the principles underpinning the new IFRS 9 / CECL standards

Methodology We setup stylized calculations for a credit portfolio with the following main parameters and assumptions:

A portfolio of 200 commercial loans of uniform size and credit quality Maturities extending from one to five annual periods A stylized transition matrix producing typical multiyear credit curves Correlation between assets typical for a single business sector and geography portfolio Focusing on PnL estimates one year forward, with PnL being impacted both by Realized Losses (defaults) and Provision variability (both positive and negative).

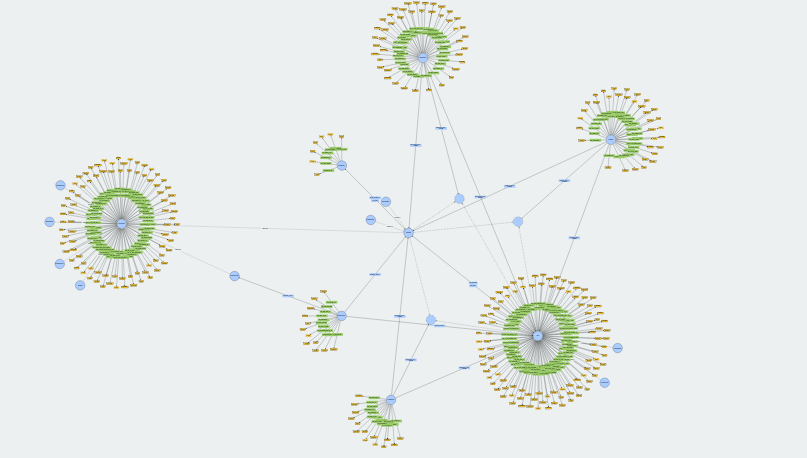

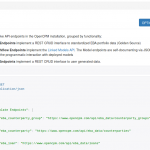

Extending the Open Risk API to include the EBA Portfolio Data Templates The Open Risk API provides a mechanism to integrate arbitrary collections of risk data and risk modelling resources in the context of assessing and managing financial risk. It is based on two key technologies of the modern Web, RESTful architectures and Semantic Data.

OpenNPL, the credit portfolio management platfrom we launched recently fully integrates the latest versions of the Open Risk API.

Credit Portfolio Management in the IFRS 9 / CECL and Stress Testing Era The post-crisis world presents portfolio managers with the significant challenge to asimilate in day-to-day management the variety of conceptual frameworks now simultaneously applicable in the assessment of portfolio credit risk:

The first major strand is the widespread application of regulatory stress testing methodologies in the estimation of regulatory risk capital requirements The second major strand is the introduction of new accounting standards (IFRS 9 / CECL) for the measurement and disclosure of expected credit losses While both Regulatory Stress Testing and IFRS 9 / CECL accounting require investment in analytic capabilities and provide unique new insights, both are aimed at satisfying evolving prudential or investor disclosure requirements.

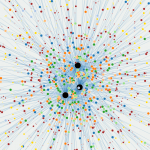

Release of version 0.3 of the ConcentrationMetrics Library Further building out the OpenCPM set of tools, we release version 0.3 of the ConcentrationMetrics Library. This python library for the computation of various concentration, diversification and inequality indices.

The below list provides documentation URL’s for each one of the implemented indexes

Atkinson Index Concentration Ratio Berger-Parker Index Herfindahl-Hirschman Index Hannah-Kay Index Gini Index Theil Index Shannon Index Generalized Entropy Index Kolm Index The image illustrates a simple use of the library where the HHI and Gini indexes are computed and compared for a range of randomly generated portfolio exposures.

Motivation for Building an open source database based on EBA’s Standardized NPL Templates In an insightful recent piece, “Overcoming non-performing loan market failures with transaction platforms”, Fell et al. dug deeply into the market failures that help perpetuate the Non-performing loan (NPL) problem. They highlight, in particular, information asymmetries and the attendant costs of valuing NPL portfolios as key obstacles. In the same wavelength, the European Banking Authority published standardized NPL data templates as a step towards reducing the obstacles that prevent the reduction of NPL’s.

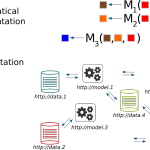

From Big Data, to Linked Data and Linked Models The big data problem:

As certainly as the sun will set today, the big data explosion will lead to a big clean-up mess How do we know? It is simply a case of history repeating. We only have to study the still smouldering last chapter of banking industry history. Currently banks are portrayed as something akin to the village idiot as far as technology adoption is concerned (and there is certainly a nugget of truth to this).

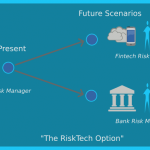

Risk Management Skills for the Fintech Era Financial services jobs continue being decimated. A recent (as of the initial post date) FT article was a sobering summary of the continuing transformation of the financial sector: 2015 alone has seen more than 10% reduction of the total workforce across large EU/US banks:

As main drivers for this true jobs hecatomb are cited higher minimum capital requirements (that depress Return on Equity and hence require lower costs to restore it to investor acceptable levels), low interest rates that erode Profitability Margins, and a generally subdued economic landscape which reduces Volumes.

Open Source Risk Data with MongoDB and Python Open source software is all the rage those days in IT and the concept is making rapid inroads in all parts of the enterprise. An earlier comprehensive survey by Gartner, Inc. found that by 2011 more than half of organizations surveyed had adopted open-source software (OSS) solutions as part of their IT strategy. This percentage may have currently exceeded the 75% mark according to open source advisory firms.