Solstice is a flexible open source economic network simulator. Its primary outcomes are quantitative analyses of the behavior of economic systems under uncertainty. In this post we provide a first overall description of Solstice to accompany the first public release.

Modeling economic networks and their dynamics Economic networks are the primary abstractions though which we can conceptualize the state (condition) and evolution of economic interactions. This simply reflects the fact that human economies are quite fundamentally systems of interacting actors (or nodes in a network) with transient or more permanent relations between them.

In practice the network character of an economy is frequently suppressed or under-emphasized and does not play a particularly important role.

Save the AMA whale ΝΒ: This is not a post about real whales and the ongoing struggle to keep these magnificent mammals alive for future generations to marvel at. Hopefully the individuals who have risked their lives to bring the near extinction of many whale species to worldwide attention will not take offense with us usurping imagery linked to this valiant campaign. We simply want to draw attention to another, rather more armchair type of campaign, namely: saving the_AMA risk model.

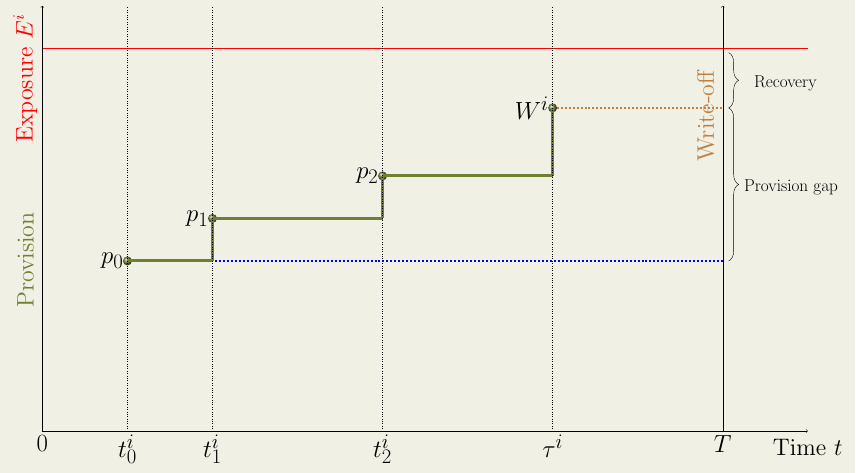

Open Risk White Paper 7: Risk Capital for Non-Performing Loans We develop a conceptual framework for risk capital calculation for portfolios of non-performing loans. In general banking practice, loans that pass a threshold of delinquency are declared non-performing and are provisioned. Yet there is a residual risk that the provisioning is not sufficient. This risk must be covered by capital buffers. The literature for risk capital requirements for NPL portfolios is very limited, which implies that Stress Testing and Internal Capital Adequacy Assessment (ICAAP) requirements for non-performing loans are harder to meet.

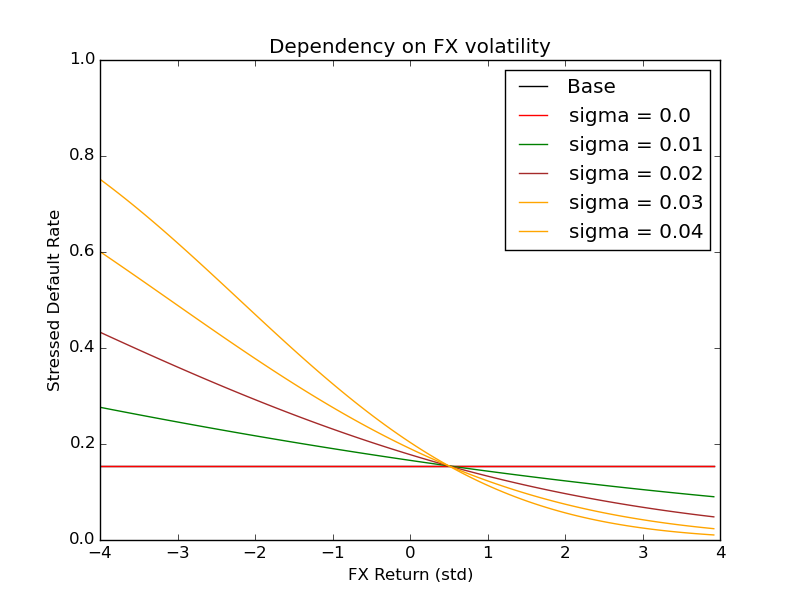

Open Risk White Paper 6: Stress Testing Methodology for FX Lending We develop a simple methodology for stress testing portfolios of credit instruments classified as foreign exchange lending. Loans whose repayment schedule is denominated in a currency other than that of the borrower’s domestic currency are commonly seen in many jurisdictions and have a risk profile that is considerably more complicated than domestic currency loans. Yet the literature for credit risk assessment and stress testing of portfolios of such loans is very limited, which means that Stress Testing and Internal Capital Adequacy Assessment (ICAAP) requirements are harder to meet.

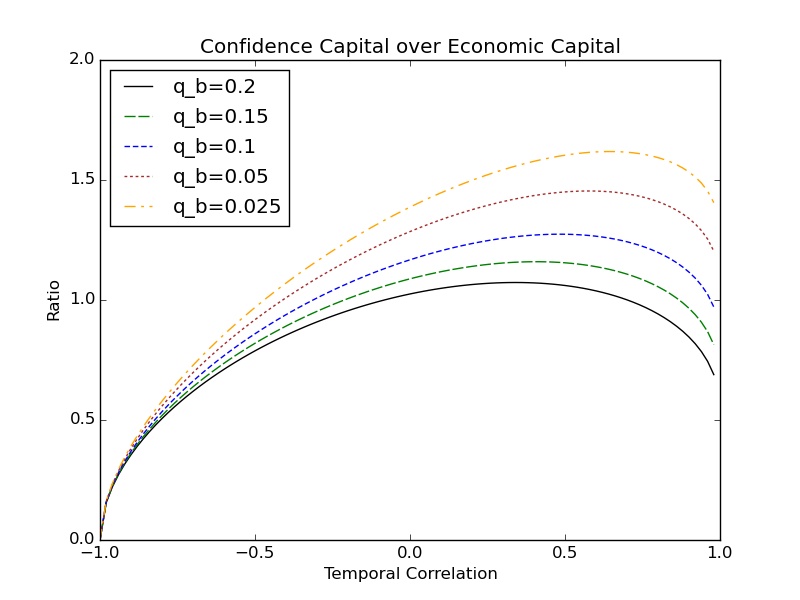

Open Risk White Paper 2: Confidence Capital: The Principle We review the structure of economic capital frameworks commonly used within financial institutions and identify why the derived capital metrics do not explicitly address the needs for maintaining ongoing confidence on the soundness of the firm. In the follow-up to the financial crisis the need for more explicit such tests has been highlighted by regulatory stress testing methodologies.

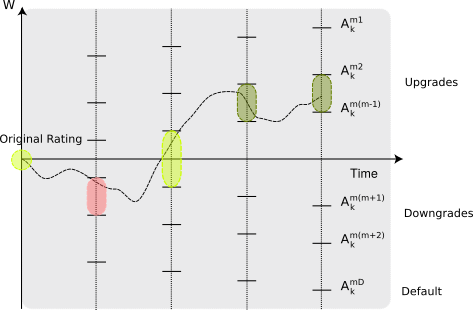

The likelihood and severity of a future ratings downgrade (as opposed to a default within the risk horizon) are the two key new risk appetite inputs required for the framework.

The mystery of the collapsed cathedral You walk to the center of an old city, and you see its glorious cathedral lying in ruins. What in the world has happened here? Your investigative instinct goes into overdrive. This is not supposed to happen. Not in peacetime anyway. How can it be that this magnificent edifice, after gracing the town’s central square for who knows how many centuries, is now little more than a rubble pile in the center of town?

Visualizing the Stress of US Banks A recurring cycle of regulatory stress testing exercises has become the new normal in the banking world, at least on the two shores of the northern Atlantic. The periodicity of the European stress testing heartbeat has not yet been firmly established. Did we just miss a beat in 2015 (a so called palpitation) or will the European cycle have two (or more) years periodicity? Who knows.

We are happy to publish the first installment of a trilogy that focuses on the risk factors that can turn any credit portfolio toxic.

The first topic is default correlation, a topic that is both core to understanding credit risk and much misunderstood.

Enjoy!

The Stress Test Explorer is a web app developed by Open Risk to assist with the exploration and understanding of the large number of results published by the European regulatory authorities (ECB/EBA) in connection with the 2014 Comprehensive Assessment exercise. The app is now live and freely accessible here.

Please note: The app is requires a modern browser to display graphics

In line with the beta testing status of the entire Open Risk website, this app may evolve, subject to user comments and feedback.

The rationale for continuing with internal capital models in the Basel 3 world Overview of the challenges and opportunities offered by internal capital models (economic capital models) in the post-crisis era. Conference Presentation given at:

Venue: 2nd Annual Capital Modelling under Basel III (Marcus Evans Conference) Location: London Time: January 28th 2014 Link to presentation: Local file