Is the IFRS 9 or CECL standard more volatile? Its all relative Objective In this study we compare the volatility of reported profit-and-loss (PnL) for credit portfolios when those are measured (accounted for) following respectively the IFRS 9 and CECL accounting standards.

The objective is to assess the impact of a key methodological difference between the two standards, the so-called Staging approach of IFRS 9. There are further explicit differences in the two standards.

Release of version 0.4 of the Concentration Library adds Geographic / Industrial concentration indexes Further building out the OpenCPM set of tools, we release version 0.4 of the Concentration Library, a python library for the computation of various concentration, diversification and inequality indices.

The below list provides documentation URL’s for each one of the implemented classic indexes (the Hoover index is a new addition in this release)

Atkinson Index Hoover Index Concentration Ratio Berger-Parker Index Herfindahl-Hirschman Index Hannah-Kay Index Gini Index Theil Index Shannon Index Generalized Entropy Index Kolm Index An important new direction that appears first in this release is the introduction of indexes that measure geographical and industrial concentration.

Representing economic activity using pictograms Visualization can produce significant new insights when applied to quantitative data. It is currently undergoing a renaissance that mirrors other developments in computing and data science. Sophisticated open source libraries such as d3.js or matplotlib, to name but a couple, are enabling an ever wider range of users to distill valuable information from the avalanche of data being produced.

Yet when it comes to visualizing data that relate to abstract concepts it can be quite difficult to find an appropriate grammar to express the quantitative context.

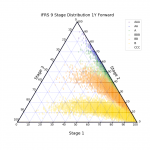

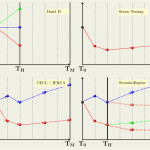

Credit Portfolio PnL volatility under IFRS 9 and CECL Objective We explore conceptually a selection of key structural drivers of profit-and-loss (PnL) volatility for credit portfolios when profitability is measured following the principles underpinning the new IFRS 9 / CECL standards

Methodology We setup stylized calculations for a credit portfolio with the following main parameters and assumptions:

A portfolio of 200 commercial loans of uniform size and credit quality Maturities extending from one to five annual periods A stylized transition matrix producing typical multiyear credit curves Correlation between assets typical for a single business sector and geography portfolio Focusing on PnL estimates one year forward, with PnL being impacted both by Realized Losses (defaults) and Provision variability (both positive and negative).

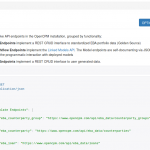

Extending the Open Risk API to include the EBA Portfolio Data Templates The Open Risk API provides a mechanism to integrate arbitrary collections of risk data and risk modelling resources in the context of assessing and managing financial risk. It is based on two key technologies of the modern Web, RESTful architectures and Semantic Data.

OpenNPL, the credit portfolio management platfrom we launched recently fully integrates the latest versions of the Open Risk API.

Credit Portfolio Management in the IFRS 9 / CECL and Stress Testing Era The post-crisis world presents portfolio managers with the significant challenge to asimilate in day-to-day management the variety of conceptual frameworks now simultaneously applicable in the assessment of portfolio credit risk:

The first major strand is the widespread application of regulatory stress testing methodologies in the estimation of regulatory risk capital requirements The second major strand is the introduction of new accounting standards (IFRS 9 / CECL) for the measurement and disclosure of expected credit losses While both Regulatory Stress Testing and IFRS 9 / CECL accounting require investment in analytic capabilities and provide unique new insights, both are aimed at satisfying evolving prudential or investor disclosure requirements.

The new IFRS 9 financial reporting standard IFRS 9 (and the closely related CECL) is a brand new financial reporting standard developed and approved by the International Accounting Standards Board (IASB).

Strictly speaking IFRS 9 concerns only the accounting and reporting of financial instruments (e.g. bank loans and similar credit products). Yet the introduction of the IFRS 9 standard has significant repercussions beyond financial reporting, and touches e.g., bank risk management as well.

What are European Safe Bonds? While the creation of the eurozone was a landmark of the European integration process, the financial crisis highlighted that the eurozone remains an incomplete design which can lead to unpredictable and adverse situations in the event of a (the) next major crisis. One of the key such incompleteness features of the current eurozone architecture is that it does not have a truly risk-free (safe) euro debt instrument: one that continues being serviced (avoids a default event) at virtually any point in time and state of the world, no matter how severe.

Release of version 0.3 of the ConcentrationMetrics Library Further building out the OpenCPM set of tools, we release version 0.3 of the ConcentrationMetrics Library. This python library for the computation of various concentration, diversification and inequality indices.

The below list provides documentation URL’s for each one of the implemented indexes

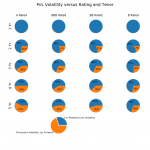

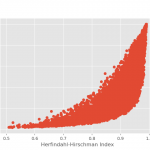

Atkinson Index Concentration Ratio Berger-Parker Index Herfindahl-Hirschman Index Hannah-Kay Index Gini Index Theil Index Shannon Index Generalized Entropy Index Kolm Index The image illustrates a simple use of the library where the HHI and Gini indexes are computed and compared for a range of randomly generated portfolio exposures.

Motivation for Building an open source database based on EBA’s Standardized NPL Templates In an insightful recent piece, “Overcoming non-performing loan market failures with transaction platforms”, Fell et al. dug deeply into the market failures that help perpetuate the Non-performing loan (NPL) problem. They highlight, in particular, information asymmetries and the attendant costs of valuing NPL portfolios as key obstacles. In the same wavelength, the European Banking Authority published standardized NPL data templates as a step towards reducing the obstacles that prevent the reduction of NPL’s.

Data Scientists Have No Future The working definition of a Data Scientist seems to be in the current overheated environment:

doing whatever it takes to get the job done in a digital #tech domain that we have long neglected but which is now coming back to haunt us!

That is nice urgency while it lasts, but it is not a serious job description for the future.

You will always find entrepreneurial institutions to offer degrees and certifications on the latest trending hashtag.

Four individuals that can look straight into your eyes Here are four individuals that can look straight into your eyes

Torvalds developed the #linux operating system, the software engine now powering anything from the tiniest #raspberrypi to the scariest supercomputer. Humanity’s best guarantee that the digital era remains an equal playing field Mullenweg developed the #wordpress blogging platform. Gave voice and content ownership to millions of digital authors making him the closest to the Gutenberg of our era Dougiamas developed #moodle, the world’s digital Academy.

Machine Learning Ballyhoo Are you getting a bit tired with all the machine learning ballyhoo?

You can blame it all on a German mathematician(*), Carl Friedrich Gauss, who started the futuristic mega-trend back in 1809: He showed us how to train a straight line to pass nicely through a cloud of unruly, scattered data points. To find, in effect, a path of least embarrassment.

Two+ centuries later it is still a profitable enterprise to invent elaborate variations of that theme, now going under the more exalted name of supervised learning, which may or may not include deep learning.

If programming languages were human languages which one would be which? Most developers know (or get to know quickly once they join a team) that programming languages are as much about communicating with other developers as they are about instructing the computer. Which raises the interesting question: If programming languages were human languages which one would be which? Here is a (tonque-in-cheek mind you!) compilation of a mapping between programming languages and human languages.

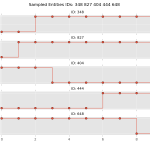

Transition Matrix Library First Release Open Risk released version 0.1 of the Transition Matrix Library

Motivation State transition phenomena where a system exhibits stochastic (random) migration between well-defined discrete states (see picture below for an illustration) are very common in a variety of fields. Depending on the precise specification and modelling assumptions they may go under the name of multi-state models, Markov chain models or state-space models.

In financial applications a prominent example of phenomena that can be modelled using state transitions are credit rating migrations of pools of borrowers.

The Zen of IFRS 9 Modeling At Open Risk we are firm believers in balancing art and science when developing quantitative risk tools. The introduction of the IFRS 9 and CECL accounting frameworks for reporting credit sensitive financial instruments is a massive new worldwide initiative that relies in no small part on quantitative models. The scope and depth of the program in comparison with previous similar efforts (e.g. Basel II) suggests that much can go wrong and it will take considerable time, iterations, communication and training to develop a mature toolkit that is fit-for-purpose.

Loan Level Templates Using Python In this Open Risk Academy course we figure step by step how to use python to work with Loan Level Templates, using the ECB SME template as an example.

Overview of the loan level template Manipulating spreadsheets with Python The Python Dictionary Organization of Portfolio Data Generating Test Portfolios Get an Open Risk Academy account and get started with the course here

This blog has been verified by Rise: Rcf8d5e45f6964ba5d03bda4020a97dda

Guiding principles for a viable open source operational risk model (OSORM) Such a framework:

Must avoid formulaic inclusion of meaningless risk event types (e.g., legal risk created by the firm’s own management decisions) or any risks where the nature and state of current knowledge does not support any meaningful quantification. Such potential risks would be managed outside the framework Must employ a bottom-up design that addresses the risk characteristics of simpler business units first and (if needed) creates a combined profile for a more complex business in a building block fashion.

The data privacy genie is out of the bottle From Yahoo’s massive email data leaks, to Equifax’s exposing of sensitive data for a large segment of the US population, to Apple’s resisting the bypassing the security features of the iPhone, not a week goes by without some alarming piece of news around data privacy.

The ramifications for the legal use of private digital data by companies and government and the consequences of illegal or unintended use are huge.

RegNews Upgrade and Dashboard Integration The Financial Regulatory News app (RegNews in short) is now integrated with the Open Risk Dashboard. The latest release adds several new feeds and allows filtering of news items by freshness (last day, last week, last two weeks) and by world-region (Supra-national, Americas, Europe and Middle East and Asia/Pacific).

As always feedback on the features and usability of the RegNews app are welcome (simply use the button!